How Mobile Wallet Passes Increase Direct Bookings for Hotels

OTAs take 15–30% per booking. Here's how mobile wallet passes shift guests to direct — and keep them there. A practical guide for independent hotels.

Every booking that comes in through Booking.com or Expedia costs your hotel between 15% and 25% of the room rate — before you factor in payment processing fees, virtual card costs, and any rate-matching concessions. The same room sold directly costs approximately 4–5% in total. That difference — 10 to 20 percentage points per booking — is one of the most significant levers an independent hotel has for protecting its profit margin. And most hotels are not pulling it hard enough. The challenge with direct booking strategies is sustaining them. It is relatively straightforward to persuade a guest to book direct on their first visit, through a best-rate guarantee, a direct-only perk, or a well-placed Google Hotel Ads campaign. The harder problem is ensuring that the same guest books direct on their second visit — and their third — rather than defaulting back to the OTA where they originally found the property. Mobile wallet passes address this problem directly, through a mechanism that most hotel direct booking guides have not yet identified: the pass creates a persistent, post-stay communication channel between the hotel and the guest that OTAs cannot replicate. This post explains the five specific ways wallet passes drive direct bookings, with the commercial data to support each one.

The Real Cost of OTA Dependency — and the Direct Booking Gap

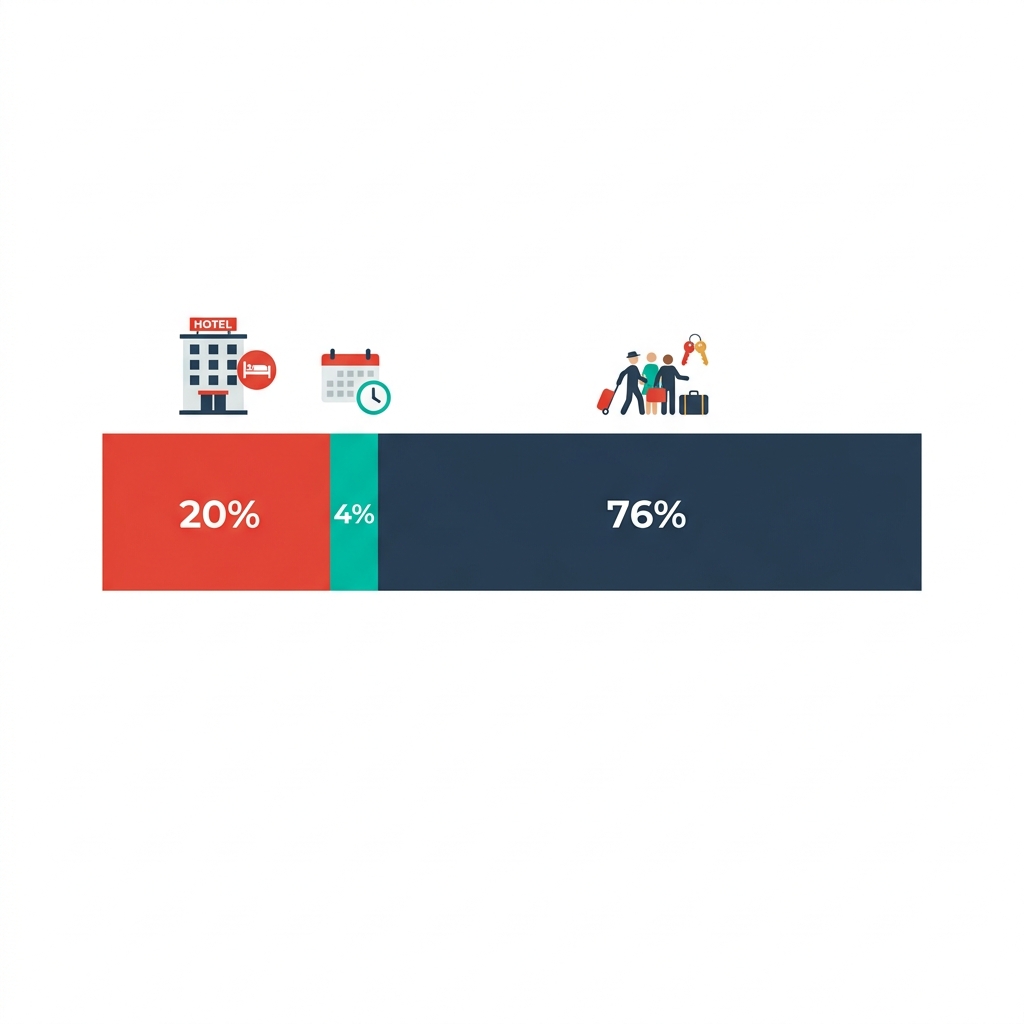

Before mapping how wallet passes increase direct bookings, it is worth establishing what is at stake financially. The headline commission rate understates the true cost of an OTA booking. DeltaHQ's 2025 analysis of OTA agreements identifies the full cost components: • Base commission: 15–18% (Booking.com), 18–25%+ (Agoda, Expedia depending on participation level) • Virtual credit card processing fee: 1.5–3% additional on top of commission (applied when OTA pays via virtual card rather than bank transfer) • Rate parity compliance costs: implicit — limiting ability to offer genuine best-rate incentives on direct channels • Guest data: retained by the OTA — the hotel receives a name and check-in date but not the email, preference, or behavioural data needed to build a direct relationship Contrast this with a direct booking. The total cost — booking engine fee, payment gateway, and proportional share of direct marketing spend — averages 4–5%. The profit margin advantage on a direct booking versus an OTA booking is 10–25 percentage points, depending on which OTA and which rate plan. Industry data from Zuzuhospitality cites direct bookings generating up to 60% higher revenue per booking than OTA reservations — the result not just of lower distribution cost, but of direct bookers consistently choosing higher-value rooms, longer stays, and more ancillary add-ons when they feel in a direct relationship with the property.

The BENELUX context: RoomRaccoon's 2024 European Booking Channel Trends Report found that in BENELUX and DACH markets, direct booking channels already outperform Booking.com as the leading source of reservations. For independent hotels in the Netherlands and Belgium, the direct booking infrastructure investment is not speculative — it is the channel where the market is already heading. Wallet passes accelerate that trajectory.

Why Most Direct Booking Strategies Fail to Retain the Guest

Standard direct booking strategies — best-rate guarantees, direct-only perks, metasearch campaigns — are effective at capturing the first booking. The problem is the post-stay gap. After checkout, the hotel's communication with the guest typically consists of: • One post-stay email asking for a review (open rate: approximately 22% genuine, as explored in Post #4 of this series) • Possibly a return discount email that competes against every other marketing message in the guest's inbox • Nothing else The OTA, by contrast, retains the guest's email, their search history, their review activity, and their booking patterns. When the guest searches for their next hotel — potentially in the same city, possibly at the same property — the OTA is already there with a recommendation, a competitive price, and a loyalty points reminder. The hotel that provided the actual stay has one email in the guest's promotions folder. This asymmetry is the real structural problem in independent hotel direct booking strategy. It is not a marketing spend problem — it is a communication channel problem. The hotel does not have a persistent, post-stay presence on the guest's device. The wallet pass changes that.

OTA vs Direct vs Direct + Wallet Pass: A Three-Way Channel Comparison

The table below frames the fundamental difference between the three booking channel models from the hotel's perspective: **Booking Channel:** OTA (e.g. Booking.com) **Revenue Retained:** 70–85% (15–30% commission deducted) **Guest Data Owned?:** No — OTA owns guest data **Rebooking Channel Available?:** No — OTA retains the relationship **Booking Channel:** Direct (website / phone) **Revenue Retained:** 95–96% (4–5% payment & tech costs) **Guest Data Owned?:** Yes — hotel owns all guest data **Rebooking Channel Available?:** Limited — email only, if opted in **Booking Channel:** Direct + Wallet Pass **Revenue Retained:** 95–96% (same as direct) **Guest Data Owned?:** Yes — full guest data + pass engagement data **Rebooking Channel Available?:** Yes — push notification channel to lock screen, persists post-stay The critical column is the third: 'Rebooking Channel Available?' An OTA-originated booking leaves the hotel with no post-stay communication channel to the guest. A direct booking without a wallet pass leaves the hotel with email — valuable, but subject to inbox competition and declining genuine engagement rates. A direct booking with a wallet pass gives the hotel a persistent, updateable, push-notification-capable presence on the guest's device that survives long after the stay ends.

Five Specific Mechanisms: How Wallet Passes Drive Direct Bookings

The following five mechanisms explain how a wallet pass programme — deployed through a platform such as tiketo — generates direct booking uplift at both the first-stay and repeat-stay stages of the guest relationship: **Mechanism 1: Pass delivery at direct booking confirmation** The wallet pass is delivered exclusively to guests who book direct — making it a tangible, immediately visible benefit of the direct booking decision. OTA bookers receive a standard confirmation email with no pass. Direct bookers receive the same confirmation plus a branded pass in their Apple Wallet or Google Wallet, with their name, booking reference, and a direct-only welcome benefit visible on the pass face. This creates an immediate, experiential difference between the two booking channels from the guest's perspective — not a vague promise of better service, but a concrete digital object that is already more functional and more personal than the OTA confirmation they received on a previous stay. **Mechanism 2: Direct-only pass benefits** Hotels can configure their wallet pass to display benefits that are only available to direct bookers: a complimentary early check-in window, a welcome drink at arrival, room upgrade priority when availability exists, or a guaranteed loyalty points multiplier on ancillary spend. These benefits are displayed on the pass face — visible every time the guest opens their wallet — and clearly labelled as exclusive to direct booking members. Skift data cited in GuestCentric's 2025 analysis found that hotels highlighting direct booking perks see a 20% higher conversion rate than those relying on price alone. The wallet pass is the most visible and persistent way to communicate those perks across the full stay lifecycle. **Mechanism 3: Post-stay loyalty pass with return incentive** At checkout, the guest's stay pass converts automatically to a loyalty pass format. The pass face updates to show the guest's accumulated points balance, their loyalty tier (or first-time member status), and a personalised return incentive — a fixed discount, a complimentary room night after a set number of stays, or a specific package offer. Ten days post-checkout, a push notification fires to the guest's lock screen: 'Your return offer expires in 50 days.' The hotel has a direct line to the guest's device — not their email inbox, but their lock screen — without competing against hundreds of other promotional emails. The return incentive links directly to the hotel's direct booking engine, not to any OTA. **Mechanism 4: Loyalty tier tied exclusively to direct bookings** Hotels using a tiketo loyalty pass can configure the points system so that direct bookings earn full points while OTA bookings earn reduced or no points. This is the same mechanism large chains use with their own loyalty programmes — Marriott Bonvoy and Hilton Honors both offer significantly fewer or zero loyalty points on OTA-originated bookings — but made accessible to independent hotels without enterprise infrastructure. Over the course of two or three stays, a guest who began on an OTA has a clear financial incentive to migrate to direct booking: the points accumulation visible on their pass is growing only when they book direct. The pass makes this comparison visible and persistent in a way that an email loyalty programme cannot replicate. **Mechanism 5: Geo-triggered ancillary spend during the stay** This mechanism is less direct in its rebooking impact but significant for the total value of the direct booking relationship. Geo-triggered notifications during the stay — a lunchtime spa promotion, an evening restaurant alert, a late-checkout offer on the final morning — generate ancillary revenue that increases the total yield from the direct booking. Higher total stay value strengthens the ROI case for the direct channel and gives the hotel more resource to invest in direct booking incentives.

Compounding effect: Each of these five mechanisms individually produces a measurable direct booking uplift. Operating simultaneously, they create a compounding effect: the pass makes the direct booking decision visible and rewarding, the loyalty tier creates a growing financial incentive to return direct, and the post-stay push keeps the hotel present on the guest's device until they are ready to book again. OTAs compete for that moment of rebooking decision. A hotel with an active wallet pass programme is already there.

A Worked ROI Example: What the Numbers Look Like

To illustrate the commercial impact, consider an independent 3-star hotel in Amsterdam with an average room rate of €140 and 60% of bookings currently originating from OTAs at an average 20% commission. **Current state (without wallet pass direct booking programme)** • 100 bookings per month: 60 via OTA (€140 × 80% net = €112 per booking), 40 direct (€140 × 96% net = €134.40 per booking) • Monthly net room revenue: (60 × €112) + (40 × €134.40) = €6,720 + €5,376 = €12,096 **Target state (with wallet pass programme, 15% direct booking shift)** • After 12 months with an active wallet pass loyalty programme driving direct rebooking: 51 OTA bookings, 49 direct (a 15-booking shift from OTA to direct, representing a conservative 25% improvement in direct share) • Monthly net room revenue: (51 × €112) + (49 × €134.40) = €5,712 + €6,585.60 = €12,297.60 • Monthly revenue uplift from channel shift alone: +€201.60 per month, or approximately €2,419 annually • Additional uplift from 15–20% ancillary revenue increase in direct bookings (driven by in-stay wallet pass upsells): estimated +€800–€1,200 annually at conservative in-stay conversion rates • Total estimated annual revenue benefit: €3,200–€3,600 from a 60-room property with modest improvements in direct share This calculation excludes the guest lifetime value compound: each direct booking that generates a loyalty pass relationship is a guest who has a higher probability of returning direct on their next stay, further improving the OTA:direct ratio over a 24–36 month horizon.

Important note on attribution: These figures illustrate the mechanism and order of magnitude; actual results depend on property size, rate tier, guest mix, and pass adoption rates. Hotels using tiketo typically track direct booking attribution through UTM parameters on the wallet pass return incentive link and through PMS rebooking source codes. Accurate measurement is built into the implementation.

Real-World Example: Shifting the OTA Mix at a 4-Star Hotel in Valencia

A 4-star hotel in Valencia with 72 rooms was generating approximately 55% of bookings via OTAs, primarily Booking.com. Their average Booking.com commission rate was 17%. They had no post-stay communication programme beyond a generic review request email. After implementing a tiketo wallet pass programme with a direct-booking loyalty pass, they made three specific changes: 1. Pass delivered exclusively to direct bookers at confirmation, displaying a 'Direct Member' badge and three direct-only perks (free late check-out to 1pm, welcome drink, and double points on F&B spend). 2. At checkout, the pass converted to a loyalty card with a tiered points system: direct bookings earned 10 points per euro of room revenue; OTA bookings earned 0 points. The guest's current balance and tier progress were visible on the pass face. 3. Post-stay push notification fired 10 days after checkout with a personalised return offer linked directly to the hotel's booking engine — bypassing OTA search entirely. Over the following 12 months, the hotel's direct booking share increased from 45% to 57% of total room nights — a 12-percentage-point shift. The average revenue per direct booking also increased, driven by higher ancillary spend from guests who engaged with the in-stay pass notifications. The total financial impact was a net revenue improvement that the hotel attributed primarily to the reduction in OTA commission cost and the increase in ancillary yield from pass-active guests.

Closing Insight

The wallet pass is not a marketing gimmick — it is the missing piece of the independent hotel direct booking infrastructure. Most hotels have a website, a booking engine, and a best-rate guarantee. What they lack is a post-stay communication channel that keeps them visible and relevant on the guest's device between stays, without competing against email inbox noise or OTA retargeting campaigns. The commercial case is direct: OTA bookings cost 15–30% in real distribution fees. Direct bookings cost 4–5%. Every percentage point of direct booking share recovered from OTAs is profit margin returned to the hotel — and reinvested in the guest experience and direct booking infrastructure that drives the next shift. Ready to build a direct booking channel that survives checkout? tiketo deploys Apple Wallet and Google Wallet passes for independent hotels across Spain and Benelux — with loyalty conversion, post-stay push notifications, and direct-booking-only perks that keep your guests on the direct channel, stay after stay.

Frequently Asked Questions

Q: Can mobile wallet passes really increase direct bookings?

A: Yes — through five specific mechanisms: pass delivery exclusively at direct booking confirmation (making the channel tangibly more valuable), direct-only benefits displayed on the pass face, post-stay loyalty conversion with a direct-linked return incentive, a loyalty tier system that earns points only on direct bookings, and geo-triggered in-stay ancillary upsells that increase the total value of the direct booking relationship. Each mechanism individually produces a measurable uplift; operating simultaneously they create a compounding direct booking effect over a 12–24 month horizon.

Q: How do wallet passes help hotels reduce OTA dependency?

A: OTAs retain the guest relationship after checkout — which is why guests default back to the OTA for their next booking. A wallet pass gives the hotel a persistent post-stay communication channel that OTAs cannot replicate: a push notification to the guest's lock screen 10 days after checkout with a return incentive linked directly to the hotel's booking engine. Combined with a loyalty programme that awards points only on direct bookings, the pass creates a growing financial incentive for guests to migrate from OTA to direct over successive stays.

Q: What is the profit margin difference between direct and OTA bookings?

A: OTA commission rates for independent European hotels typically range from 15–25% per booking on major platforms, with the real cost — including payment processing, virtual card fees, and rate-matching costs — often reaching 25–30% of room revenue. Direct bookings cost approximately 4–5% in total distribution cost. The resulting profit margin advantage on a direct booking is 10–25 percentage points per room night. Industry data from Zuzuhospitality cites direct bookings generating up to 60% higher revenue per booking versus OTA reservations when accounting for full revenue per stay.

Q: Do wallet passes work for BENELUX hotels specifically?

A: Yes — and the BENELUX market is particularly favourable for wallet pass direct booking programmes. RoomRaccoon's 2024 European data found that direct booking channels already outperform Booking.com in BENELUX, making the market more direct-booking-ready than most European regions. Google Wallet dominates the Android-majority Dutch and Belgian markets, and Gmail Auto-Import (available since October 2025) makes pass adoption even more frictionless for guests with Gmail accounts — which is the majority of Android users in these markets.

Q: How long does it take to see direct booking uplift from a wallet pass programme?

A: The post-stay return incentive push notification fires 7–10 days after checkout, creating an initial conversion opportunity within the first two weeks of pass programme launch. Meaningful uplift in direct booking share typically becomes measurable within three to six months of programme operation, as the loyalty tier system begins creating compound incentive for repeat guests. The full effect — including the migration of OTA-originated guests to direct over successive stays — is best measured over a 12–24 month horizon.

More from the tiketo Blog

How to Build a Hotel Loyalty Program Without a Big Tech Budget

Independent hotels don't need enterprise software to run a loyalty programme. Here's a practical, right-sized framework — built on a wallet pass.

Mobile Check-In, Room Keys & Loyalty in One Pass: Is It Possible?

Can one digital hotel pass handle check-in, room key access and loyalty? Here's the honest answer — what's possible today, what needs hardware, and how to start.

Google Wallet Hotel Passes: The Complete Hospitality Guide

Everything hotel teams need to know about Google Wallet passes — pass types, push notifications, geo-triggers & real results. Powered by tiketo.

Apple Wallet for Hotels: How to Engage Guests Without an App

Apple Wallet is on every iPhone. Yet most hotels use it for one thing: a room door key. The pass — Apple's most powerful hospitality capability — is going almost entirely unused. Here's the full picture.

Push Notifications vs. Email: Which Works Better for Hotel Guest Communication?

If you manage guest communications at a hotel, there is a good chance you are making channel decisions based on email open rate data that is significantly inflated.

How to Personalise the Hotel Guest Experience at Scale

71% of hotel brands say personalisation is a priority, but only 15% believe they are doing it effectively. Discover a practical framework for bridging the execution gap without a full CRM overhaul.

5 Hospitality Trends Redefining the Guest Experience in 2026

From AI-powered bookings to digital wallet loyalty, discover the 5 data-backed trends redefining the guest experience in 2026 — and what they mean for your property.

How La Bottega Turns Guests Into Regulars.

Like many successful restaurants, La Bottega faced a familiar challenge: guests loved the experience, but paper loyalty cards weren't enough.

What Is a Digital Guest Journey and How to Map It for Your Hotel

Most hotels can describe what happens at check-in. Far fewer can describe what happens in the twelve touchpoints before a guest arrives, or the eight that follow after checkout. That gap is exactly what a digital guest journey map is designed to close.

Why Guests Don't Download Hotel Apps — And What to Do Instead

Over 70% of guests drop off before completing hotel app registration. Here's why — and the no-download alternatives that actually work.

Loyalty Programs for Boutique Hotels: What Actually Works

Most boutique hotels copy chain loyalty mechanics and wonder why it fails. Here's what actually works — and why your advantage is emotional, not transactional.